Discounted cash flow, or DCF, is a valuation methodology used to determine the current value of investments. It is based on the theory that an investment’s current value should equal the present value of its future cash flows.

Investments such as bonds or shares are expected to generate future cash flows in the form of interest or dividend payments. According to the DCF valuation method, the present value of an investment should be the sum of all future cash flows from that investment, discounted to take account of the time value of money.

What is the time value of money?

The time value of money is a core financial principle that means a dollar received today is worth more than a dollar received next week or next year. This is because a dollar received today can be invested and earn returns, meaning it should be worth more in the future.

This means that money expected to be received in the future is worth less than if it were received today. The present value of a sum of money to be received in the future can be determined by discounting it appropriately.

Discounted cash flow accounts for the time value of money by discounting future cash flows to determine their present value. Theoretically, by summing up the present value of all future cash flows from an investment, we can determine its current value.

To do so accurately, however, we need to estimate the future cash flows correctly and use an appropriate discount rate. The higher the discount rate used, the lower the present value of a sum of money will be. For example, if we expect to receive $1,000 in one year, its present value will be $952.38 if we use a 5% discount rate. If we use a 10% discount rate, the present value will be $909.09.

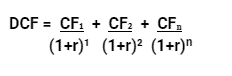

What’s the DCF formula?

CF = the cash flow for a given year: that is, CF₁ is the cash flow for year 1, CF₂ is the cash flow for year 2, and CFₙ is the cash flow for future years.

r = the discount rate.

Because the DCF model is calculated using projected future cash flows, the accuracy of these projections is key to ensuring the model’s accuracy. Using the correct discount rate is also crucial to ensure the accuracy of outputs from the DCF model.

The discount rate used in the DCF model will depend on an investor’s minimum rate of return. For example, say we offered to pay you $1,000 in one year. If the minimum rate of return you require is 5%, then you should be willing to pay us up to $952.38 now (assuming there is zero risk of us defaulting). On the other hand, if your minimum rate of return is 10%, you would only be willing to pay us up to $909.09 now.

If there is a risk we will default, you will need to adjust the discount rate accordingly. As such, there is no right or wrong rate of discount. The rate will differ between investors and will also be based on the attributes of the investment and capital market conditions.

Companies often use their weighted average cost of capital1 as the discount rate when using the DCF model to assess an investment. This is because the weighted average cost of capital accounts for returns expected by shareholders.

When would you use a DCF model?

You can apply the DCF model to any investment where you pay money now, expecting to receive money in the future. Provided the inputs into the DCF model are accurate, it can indicate whether a potential investment is over or undervalued.

Suppose the DCF model gives a result higher than the current price of the investment. This indicates the investment is undervalued and potentially worthy of consideration. If the DCF model gives a result lower than the current price of the investment, it indicates the investment may be overvalued, so you may want to look elsewhere.

Let’s look at an example. Say you are offered the opportunity to invest $1 million today, with that investment expected to generate cash flows of $250,000 per year over the next five years. The table below shows the value of the discounted value of these cash flows, assuming a discount rate of 5%:

| Year | Cash flow | Discounted cash flow |

| 1 | $250,000 | $238,095 |

| 2 | $250,000 | $226,757 |

| 3 | $250,000 | $215,959 |

| 4 | $250,000 | $205,675 |

| 5 | $250,000 | $195,881 |

If you sum up the discounted cash flows, you get a total of $1,082,369. This is more than $1 million, indicating you should consider the investment opportunity.

How would you use a DCF model?

Analysts use the DCF model to directly measure the value of an investment, as it ultimately derives its value from the inherent value of the cash that flows to investors. This means they can use the DCF model to evaluate a company’s value and compare businesses.

To evaluate a company’s value, analysts will project its cash flows over a certain period, as well as a terminal value for the business at the end of that time. They then discount the monetary values appropriately and sum them up to arrive at the present value of the business. To compare businesses, they can calculate the valuation of each using the DCF model.

What are the limitations of discounted cash flow?

There are several limitations to the DCF model. The valuation provided by the model is sensitive to the assumptions and forecasts used in generating it. Changes in these assumptions and forecasts can lead to significant differences in the results of a DCF valuation.

Because the DCF model requires predicting future events, actual outcomes may differ from those predicted. Even the best forecasters cannot predict the future with 100% accuracy, so the results of the DCF model may prove different from reality.

The DCF model also does not consider market-related information, such as the value of comparable companies. Using this information can provide a sanity check on the results of the DCF model, so it is recommended that DCF analysis be employed in conjunction with other valuation techniques. This can help ensure that inaccurate assumptions or forecasts do not result in a significantly different valuation from that indicated by market forces.

Although theoretically sound, the DCF model is sensitive to the assumptions and forecasts it relies on. Forecasting future performance is notoriously difficult, which is one of the drawbacks of using DCF. On the plus side, temporary market conditions or non-economic factors do not influence DCF. The model can also be useful when there is limited information with which to compare a potential investment.